Initiation of coverage · Consumer Internet / Online Travel

Booking Holdings Inc. (NASDAQ: BKNG)

The market is paying 17× for a business retiring 8% of itself a year.

The full 9-page research note

Model, football field, scenario table, risk matrix and disclosures. Free, no email required.

The call

I'm initiating on Booking Holdings with a BUY and a $240 target.

BKNG has de-rated to roughly 17× forward earnings — near the low end of its post-COVID history — not because the business broke, but because the market decided AI agents will make online travel agencies obsolete. Meanwhile the company just posted a record quarter of capital return and grew adjusted EPS 14% into a live geopolitical headwind.

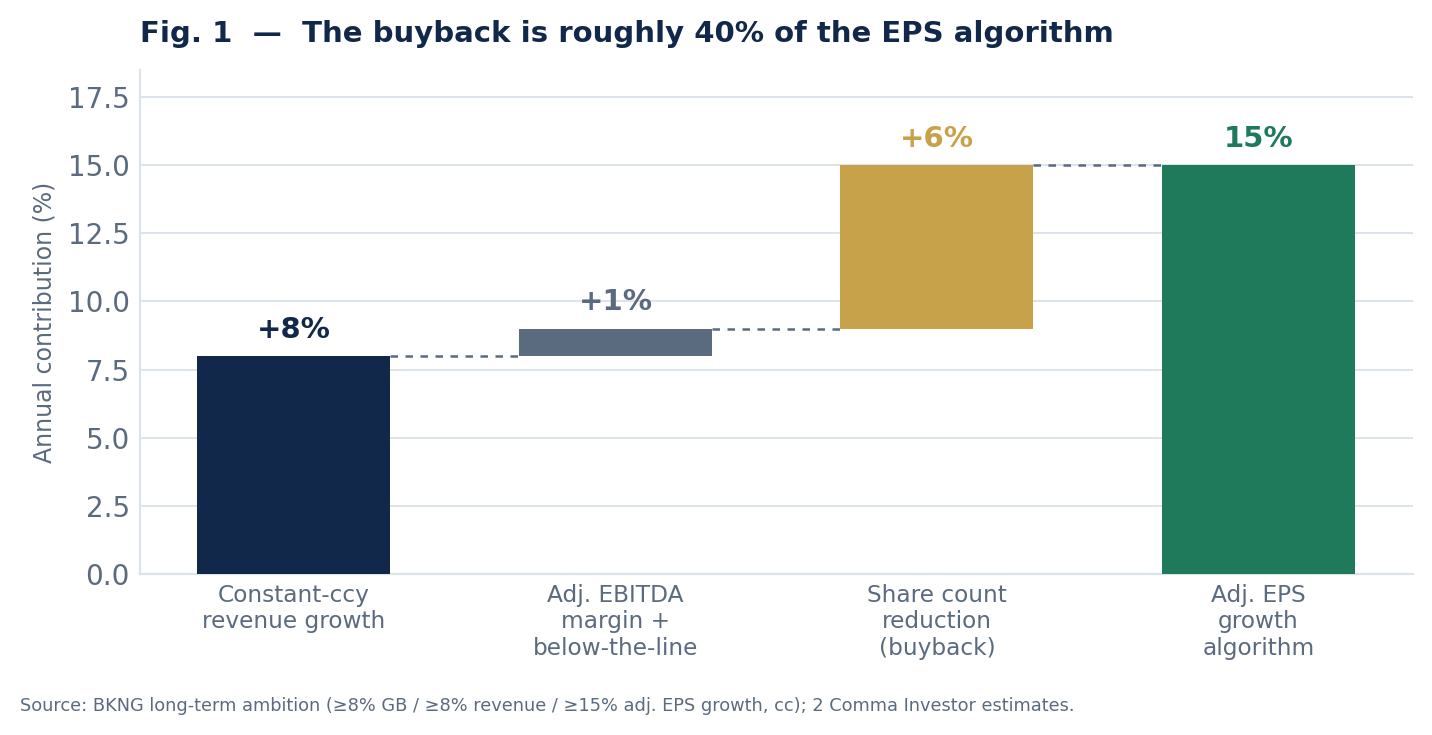

The thesis rests on three legs. One: the buyback is not a nice-to-have, it is roughly 40% of the earnings algorithm, and management is executing it at scale into weakness. Two: the growth story — merchant mix shift, Connected Trip, flights, alternative accommodations, Agoda in Asia-Pacific — is intact and being obscured by a temporary regional shock. Three: the AI bear case is directionally real but has been front-loaded into the multiple, and the first hard evidence from 2026 cuts against it.

You are being paid roughly a 9% shareholder yield to wait, with a Q2 print on July 28 as the near-term catalyst.

| Market cap | $138.2B | Forward P/E | 17.0× |

| Enterprise value | $141.2B | Trailing P/E (GAAP) | 23.5× |

| Shares out (post-split) | ~787M | PEG (5y expected) | 0.77 |

| Dividend / yield | $1.68 / 0.96% | Payout ratio | ~21% |

| Buyback authorization left | ~$18.2B | Total shareholder yield | ~8.9% |

| 52-week high | $233.58 | Below 52-wk high | –24.9% |

| 6-mo vs. S&P 500 | –26.1% | vs. 200-day MA | –6.6% |

| Street consensus | Buy (0 sells) | Street avg. target | ~$225 |

What the market is missing

The buyback is doing the heavy lifting, and nobody is pricing it

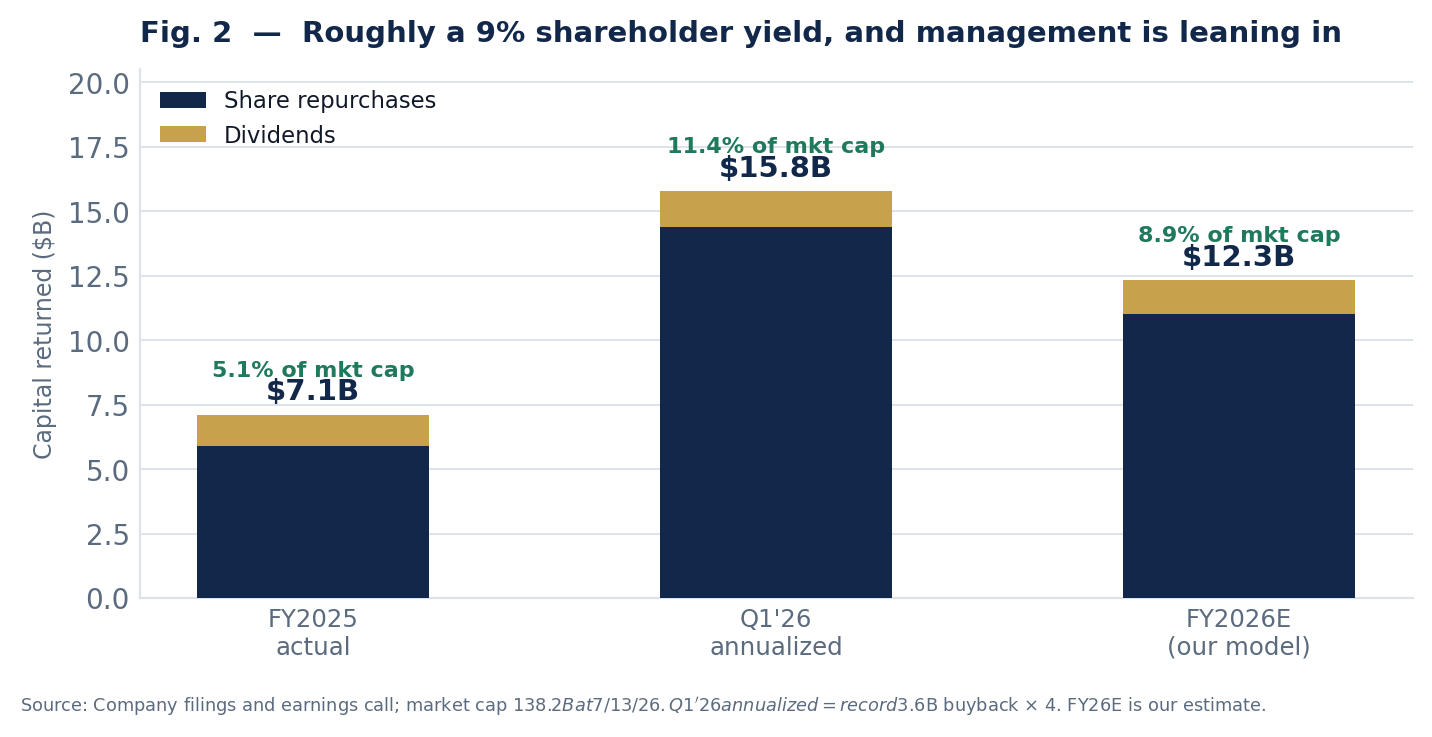

Management has retired more than 40% of shares outstanding since 2014 — net of stock comp dilution — at an average cost of roughly $93 per share (split-adjusted). The stock is $175.52. Those repurchases are sitting on an ~89% gain. In Q1 2026 alone they bought back a record $3.6B and paid $343M in dividends: about $4.0B returned in a single quarter, the largest in company history, funded by ~$3.1B of free cash flow. Roughly $18B of authorization remains — about 13% of the entire market cap.

The growth slowdown is a headline, not a trend line

Q1 room nights grew 5.9%. Strip out the Middle East conflict, which management sizes at roughly two percentage points, and the underlying number is ~8% — right on the long-term algorithm. Revenue still grew 16%. Adjusted EPS still grew 14%. Guidance assumes the drag persists through mid-year and then recovers. If it does, the compares in 2H26 get easy fast.

The AI panic ran ahead of the AI evidence

The de-rate began when Google announced agentic booking in AI Mode and accelerated on OpenAI checkout fears. But in March 2026 OpenAI pulled native checkout and re-routed purchases to third-party apps; Google has said explicitly it does not intend to take payment or hold the reservation — a named partner does. The agent still needs someone to actually transact. That someone has 2.9M properties and the payment rails.

1 · The capital return engine

Most investors underwrite BKNG as a travel-demand story. That is the wrong frame. It is a cash-conversion-and-share-shrink story that happens to sell hotel rooms. Management's own long-term ambition — at least 8% constant-currency gross bookings growth, at least 8% revenue growth, and at least 15% adjusted EPS growth — only reconciles if the share count keeps falling. It has, relentlessly.

The dividend is small, young, and growing fast

BKNG only initiated a dividend in 2024, so the yield screens poorly at 0.96% and income funds ignore it. That is a mistake of framing. In January 2026 the board raised the payout 9.4%, to $10.50 per share pre-split — $0.42 post the 25-for-1 split effected April 2. The payout ratio is roughly 21%, which means the dividend is not a constraint on anything; it is a rounding error against free cash flow. A ~1% yield growing at high-single to low-double digits off a 21% payout, from a company generating $9B+ of FCF, is a dividend-growth position that hasn't been recognized as one yet. The company distributed $1.2B in dividends across 2025.

Why this matters more at $175 than it did at $233

This is the part the AI narrative obscures. A buyback is an investment decision, and its return depends entirely on price paid. When BKNG spends $3.6B at a 17× multiple, every dollar retires ~40% more earnings than the same dollar spent at 24×. The de-rating is not purely a cost to shareholders who hold; it is a subsidy to them, provided the cash flow is durable. Management said as much on the Q1 call — they framed the repurchase program as betting on themselves at the right times, and the $93 average cost basis is the receipt.

The honest counterpoint: the balance sheet is doing some of the work. BKNG carried $15.4B of long-term debt at quarter-end and issued $750M of senior notes in Q1. Years of aggressive repurchase have pushed book equity negative, which is common for buyback-heavy compounders but does remove a shock absorber. Cash and investments of $16.5B against that debt keeps net leverage modest, and the debt fell from $16.9B at year-end — but this is a company returning more than 100% of free cash flow, and that only works while the cash flow shows up.

2 · The growth story that got buried

2025 was the fourth consecutive year of record gross bookings, room nights, and revenue. Revenue rose 13% to $26.9B. Adjusted EBITDA rose 20% to $9.9B, with margin expanding to 36.9% from 35.0%. Adjusted EPS rose 22%. Free cash flow rose 15.1% to $9.09B. This is not a company in decline; it is a company whose multiple is in decline.

Merchant mix shift — the quiet re-rating of the business model

BKNG is migrating from the agency model (traveler pays the hotel, BKNG takes a commission later) to the merchant model (BKNG is the merchant of record and collects at booking). Q1 merchant revenue grew 26.7% to $3.70B and is now 66.8% of total revenue, while agency revenue shrank 2.3%. Merchant is expected to reach ~68% of bookings in 2026. This matters three ways: it lifts the take rate, it generates float and deferred merchant bookings (a working-capital tailwind), and — critically for the AI debate — it puts BKNG in control of payments and the customer relationship rather than acting as a lead-gen referral.

Connected Trip — attach rate is the moat, not the interface

Connected Trip transactions grew over 30% YoY in Q4 2025. Airline tickets grew 37% to 68M. Multi-vertical transactions — a traveler booking flight, hotel, and car together — grew in the high-20% range. Each additional vertical raises switching costs and lifts lifetime value per user. An AI agent can recommend a hotel; assembling and servicing a four-component itinerary with one liable counterparty is a materially harder problem.

Alternative accommodations — attacking Airbnb from a position of strength

Alternative accommodation listings hit a record 8.6M in 2025 (+8%) and now represent roughly 36% of all room nights. BKNG is doing this while Airbnb absorbs urban regulatory pressure, and it does it inside the same funnel that already sells hotels — no separate acquisition cost.

Geographic hedge — Agoda and Asia-Pacific

U.S. inbound tourism has been soft, with analysts pointing to a ~6% decline in foreign visits following 2025 policy changes and a sharp drop in Canadian travel to the U.S. BKNG's strength in Asia-Pacific via Agoda, plus rising cross-border travel in China and Southeast Asia, is a structural offset that U.S.-centric peers do not have. The June 2026 FIFA World Cup is an additional North American RevPAR tailwind landing squarely in the Q2/Q3 numbers.

Cost transformation — the margin is not an accident

The 2026 transformation program is tracking to $500–550M of in-year savings, with only $25M of costs incurred in Q1. Adjusted fixed operating expenses grew low single digits on a normalized basis. Management guides adjusted EBITDA to grow slightly faster than revenue with margin up 0–25bps. AI is showing up here first — in customer service automation and marketing efficiency — which is worth remembering when the same technology is cited as the existential threat.

3 · The AI debate, adjudicated

This is the whole argument. BKNG is down ~25% over the past year and has underperformed the S&P 500 by 26 points over six months almost entirely on the belief that agentic AI disintermediates the online travel agency. I take the bear case seriously — and conclude the market has priced a structural outcome on the basis of a narrative that 2026's actual evidence has been steadily undercutting.

The bear case (fair points)

The rebuttal (what 2026 actually showed)

The conclusion. Booking Holdings has been declared dead by hotel chains taking back direct bookings, by metasearch, by voice assistants, and by blockchain. It survived each because the hard part of travel was never the search box — it was aggregating 2.9M properties, standardizing the inventory, holding the money, and eating the liability when a room is wrong at 11pm in a foreign country. Agentic AI compresses the discovery layer, which is genuinely bad for KAYAK and mildly bad for BKNG's marketing leverage. It does not build the supply side. As CFO Ewout Steenbergen framed it, the supplier proposition is “a competitive strength as agentic AI accelerates the pace of change.” I think that is right, and I think 17× says the market does not.

4 · Valuation and scenarios

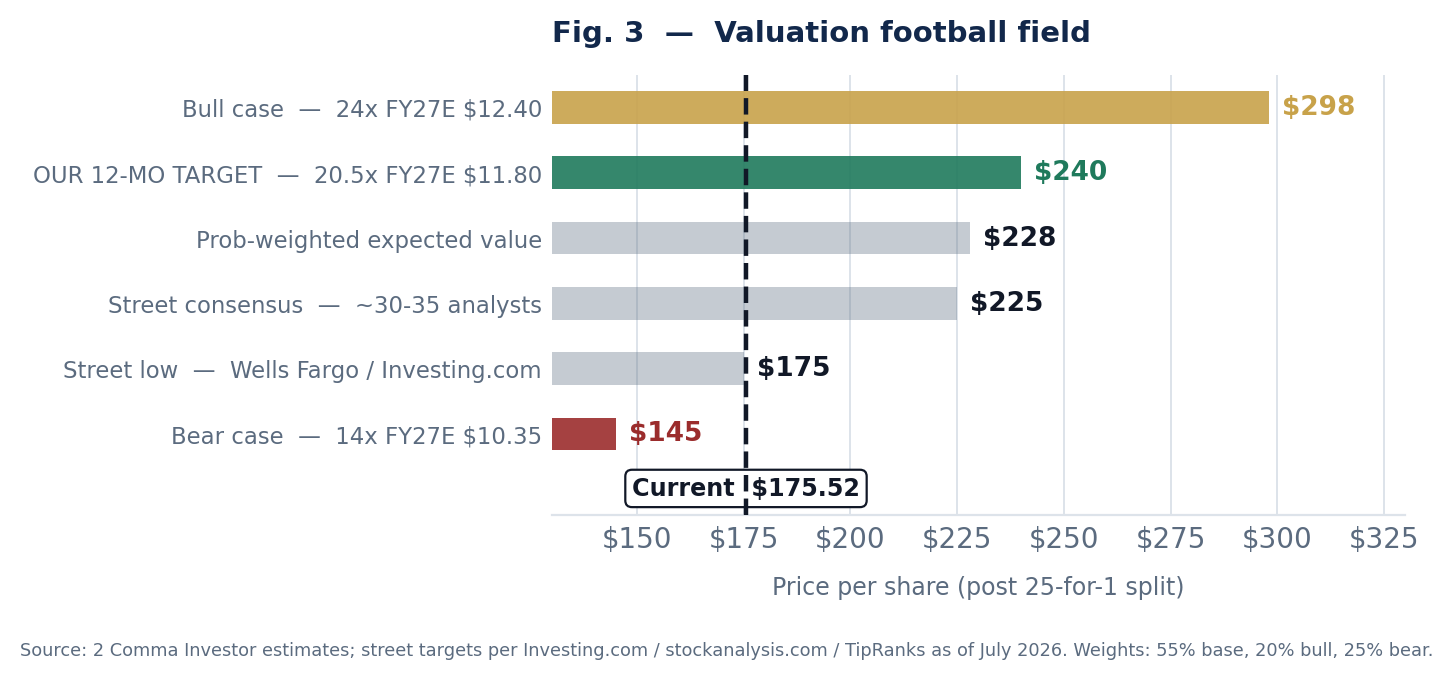

I value BKNG on forward adjusted EPS. FY25 adjusted EPS was $228.06 pre-split, or $9.12 post-split. Management guides FY26 adjusted EPS up low-to-mid teens, which lands at ~$10.35 — consistent with the 17.0× forward multiple implied at the current price. Applying the long-term 15% algorithm, haircut for regulatory and AI friction, I carry $11.80 for FY27.

| Scenario | Weight | FY27E EPS | Multiple | Value | Return | What has to happen |

|---|---|---|---|---|---|---|

| Bull | 20% | $12.40 | 24.0× | $298 | +70% | Middle East normalizes by 3Q, room nights reaccelerate to 8%+, AI fear unwinds and the multiple returns toward historical, buyback runs above $13B. |

| Base | 55% | $11.80 | 20.5× | $240 | +37% | Guidance holds. 2H recovery arrives roughly on schedule. AI stays a discovery-layer story. $10–12B of buyback shrinks the count ~7–8%. Partial multiple repair to 20.5×. |

| Bear | 25% | $10.35 | 14.0× | $145 | –17% | Conflict persists past mid-year, 2H recovery slips. Take rates begin compressing on AI-mediated volume, KAYAK impairs, DMA bites. Multiple stays structurally de-rated. |

| Weighted EV | 100% | — | — | $228 | +30% | Even carrying a 25% weight on a structurally-broken bear case, expected value sits ~30% above spot. That asymmetry is the trade. |

| Metric | FY2025A | Q1 2026A | FY2026E | FY2027E |

|---|---|---|---|---|

| Revenue | $26.9B (+13%) | $5.53B (+16%) | ~$29.2B (+9%) | ~$31.6B (+8%) |

| Adj. EBITDA | $9.9B (+20%) | — (+19%) | ~$10.8B | ~$11.8B |

| Adj. EBITDA margin | 36.9% | — | ~37.0% | ~37.3% |

| Adj. EPS (post-split) | $9.12 (+22%) | $1.14 (+14%) | ~$10.35 (+13%) | ~$11.80 (+14%) |

| Free cash flow | $9.09B (+15%) | ~$3.1B | ~$9.5B | ~$10.2B |

| Buybacks | $5.9B | $3.6B (record) | ~$11B | ~$11B |

| Dividends paid | $1.2B | $343M | ~$1.3B | ~$1.5B |

| Share count change | — | — | ~–7 to –8% | ~–7% |

| Cash & investments | $17.8B | $16.5B | — | — |

| Long-term debt | $16.9B | $15.4B | — | — |

5 · Catalysts

Q2 2026 earnings — Tuesday, July 28 (14 days out). Consensus sits at $2.44 adjusted EPS (range $2.25–$2.64) on revenue of ~$7.20B. Guidance called for room nights +2–4% and gross bookings, revenue and adjusted EBITDA each +4–6%. This is a low bar, deliberately set. Four things to watch:

- Room-night trajectory ex-Middle East. The whole 2H thesis is that the ~2pt drag is transitory. Any commentary that the recovery has begun re-rates the stock more than the EPS beat does.

- Buyback pace. Q1 was $3.6B. If Q2 comes in anywhere near $2.5–3B, the full-year number pushes toward the top of my range and the share-count math accelerates.

- Transformation savings. $500–550M of in-year savings is the margin bridge. Confirmation keeps the EBITDA guide credible.

- FIFA World Cup flow-through. The June tournament lands in this quarter and should support North American RevPAR — a rare U.S. tailwind after a soft inbound year.

Secondary catalysts: continued analyst target revisions (Argus raised to $210 on July 9); the Trade Desk partnership monetizing travel data through advertising; and any further evidence that AI platforms are settling into a referral rather than a checkout role.

6 · Risks to the thesis

| Sev. | Risk | Assessment |

|---|---|---|

| HIGH | AI disintermediation / take-rate compression | The core structural risk and the reason the stock is here. If Google or Apple ship agentic booking that clears at commissions materially below 15–20%, margins compress even on flat volume. I think this is a multi-year, not multi-quarter, question — but I am underwriting it, not dismissing it. |

| HIGH | Middle East conflict duration | Guidance explicitly assumes impacts through June followed by a 2H recovery. If the conflict extends, the FY26 adjusted EPS guide is at risk, and the story loses its cleanest bull catalyst. |

| MED | Consumer weakness | University of Michigan consumer sentiment has been running around 56.6, under the 60 level often read as recessionary. Travel is discretionary. Elevated jet fuel prices in Europe could suppress trips and stay length. |

| MED | Regulatory and tax | EU Digital Markets Act obligations, Dutch tax authority assessments reported in the billions across the sector, and ongoing data-privacy investigations. Unquantified and permanent. |

| MED | Leverage and negative book equity | $15.4B of long-term debt and years of buyback-driven negative book value. The company returns more than 100% of FCF. This is fine while cash flow compounds and becomes a problem quickly if it does not. |

| LOW | FX | Management expects FX to add roughly 2pts to gross bookings growth and ~1pt to adjusted EPS growth in FY26. A dollar reversal removes a reported-growth tailwind that is not in the constant-currency numbers. |

| LOW | Google traffic dependency | BKNG remains one of the largest performance-marketing spenders on the planet. Google is simultaneously its biggest channel and its most credible competitor — an uncomfortable structural position regardless of AI. |

The bottom line

Booking Holdings is a business that converts roughly a third of revenue into EBITDA, generates $9B+ of free cash flow, has retired over 40% of its shares since 2014 at an average cost of $93, just returned a record $4.0B in a single quarter, raised its dividend 9.4%, and is guiding to mid-teens EPS growth. It trades at 17× forward earnings because the market has decided a chatbot will replace it.

I do not think that is a 25% discount to fair value; I think it is closer to 40%. The bear case is real and I carry a 25% weight on it. The base case gets you $240. You collect ~9% a year in buyback and dividend while you wait, and the clock starts on July 28.

Rating: BUY. 12-month target: $240.

Take the full note with you

9 pages, including the complete risk matrix, methodology and sources.

Methodology, sources & disclosures

Methodology

Target price derived from a probability-weighted scenario analysis applying an exit multiple to FY2027 estimated adjusted EPS. Base-case FY27E adjusted EPS of $11.80 reflects management's stated long-term ambition of at least 15% constant-currency adjusted EPS growth, haircut for regulatory friction and AI-related take-rate risk. The 20.5× base exit multiple sits below the multiple this business has historically commanded and above the current 17.0×, reflecting partial — not full — repair of the AI de-rate. Risk/reward of 2.1:1 computed as base-case upside ($64.48) divided by bear-case downside ($30.52) from the $175.52 reference price. Shareholder yield computed as estimated FY26 buybacks plus dividends over the $138.2B market capitalization.

Primary sources

Booking Holdings Q1 2026 Form 10-Q and earnings call transcript (28 April 2026); Q4/FY2025 results release (18 February 2026); Form DEF 14A / PRE 14A (April 2026); Q1 2026 investor presentation. Market data per Yahoo Finance, Stockopedia and stockanalysis.com. Consensus estimates and price targets per Investing.com (35 analysts), stockanalysis.com (30 analysts), TipRanks and MarketBeat, July 2026. Analyst commentary referenced from Argus, Wells Fargo, Citi, BTIG and TD Cowen via TipRanks, PhocusWire and The Silicon Review. Industry context from Reuters (5 March 2026), The Information, Skift Research / McKinsey “Remapping Travel With Agentic AI” (2026), and Forbes. All figures reflect the 25-for-1 forward stock split effected 2 April 2026.

Disclosures

This report is published by 2 Comma Investor for educational and informational purposes only. It is not investment advice, and it is not a recommendation, offer, or solicitation to buy or sell any security. The author (@2commainvestor) is not a registered investment adviser, broker-dealer, or financial analyst, and no fiduciary relationship is created by reading this document.

Position disclosure: the author may hold, and may from time to time initiate or close, a position in the securities discussed. No compensation has been received from any company mentioned in exchange for this report. 2 Comma Investor has no investment banking, advisory, or business relationship with Booking Holdings Inc.

Forward-looking statements — including estimates, targets, scenario weights and probability assessments — are opinions based on information believed reliable as of the publication date. They are not guarantees. Actual results will differ, potentially materially. Estimates and consensus figures are drawn from third-party sources that have not been independently verified. Past performance does not indicate future results. Investing in equities involves risk of loss, including total loss of principal. Read the full disclosures →